your trusted real estate resource

|

Michele Sells VA

|

|

Referrals are the lifeblood of any business, and real estate is no exception. When someone you trust refers you to a service provider, you're more likely to do business with them because you know that they've been vetted by someone you know and trust.

That's why I am so grateful for the referrals I've received from my past clients. It's a wonderful feeling to know that the work I've done has been so appreciated. If you know anyone who's thinking of buying or selling a home, please don't hesitate to refer them to me. I'd be honored to help them. As an experienced real estate agent who is passionate about helping people find their dream homes, I have a proven track record of success, and I'm dedicated to providing my clients with the best possible service. I'm known for my excellent customer service and willingness to go the extra mile to help my clients achieve their goals. Thank you for your referrals! They mean the world to us.

0 Comments

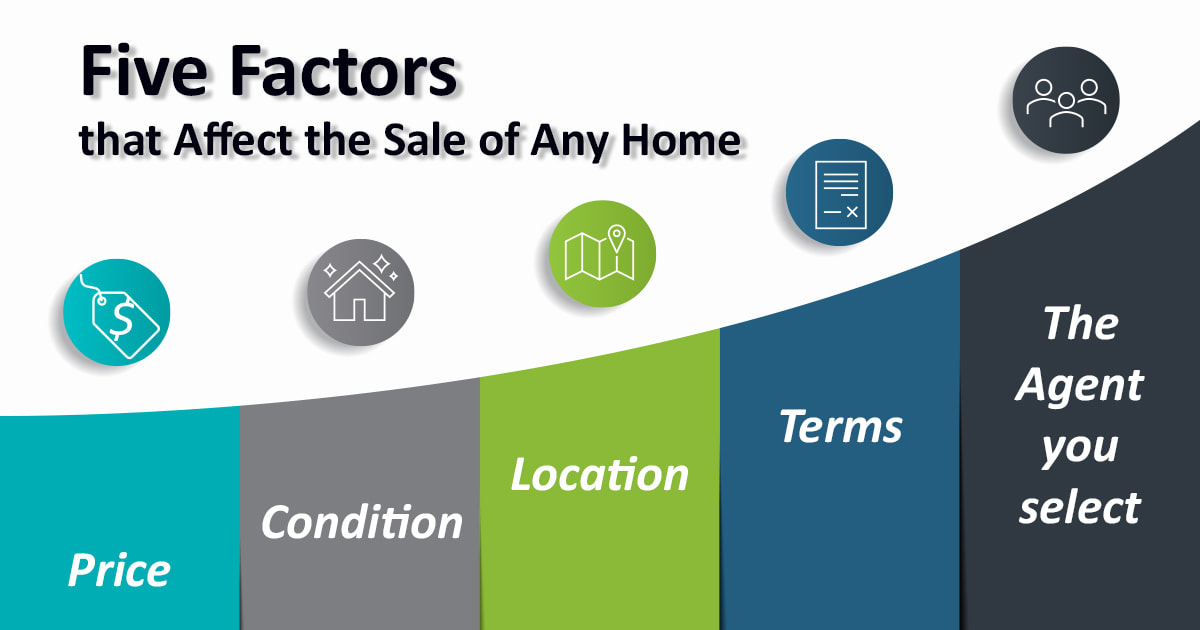

Owners directly control four of the five factors that affect the sale of any home: price, location, condition, terms, and the agent you select. The one thing you can't control is the location of the home, but you can adjust the other factors to compensate for failings.

The seller controls the price of the home which determines its positioning in the marketplace. If is priced too high, it will take longer to sell and, in some cases, for less than what it should have sold for because when it doesn't sell immediately, it is assumed that there must be an issue with it. If it is priced too low, the owner will not realize as much of their equity as they should. Not pricing the home in the proper search brackets could keep the property from being exposed to potential and likely, buyers. For example, if a home is priced at $399,000 to follow an age-old retail marketing principle, many of the most likely buyers will never know about it because they are searching for properties in the $400,000 to $450,000 range. The seller also controls the condition of a property which affects not only the marketability of a home but indirectly, the price. Homes in the best condition appeal to more buyers because for the most part, they are using their available cash for the down payment and closing costs and may not be able to afford to make cosmetic or more expensive improvements to the property. Clutter can keep buyers from seeing your home, and more importantly, it will keep them from seeing themselves in your home. There are three basic causes of clutter: there is too much stuff in the home; there is not enough space in the home; and there is no organization. Selling a home is about positioning it to sell which sometimes means temporarily or permanently getting rid of things that make the home look small or distracts the buyers from seeing its potential for them. Terms are the financial preferences established by the seller. In a competitive market with multiple bids, a seller may not have to offer any terms such as a financing, appraisal, or inspection contingencies. This will restrict the number of buyers who are financially able to pay cash and are willing to do so. In lower price range homes, there could be a wealth of qualified buyers that need to use low down payment options, closing cost assistance from the seller, or other things. When the seller consents to offer a variety of terms, the market of potential buyers increases. The seller can still select the most qualified if they are not limiting protected classes. The fourth marketing factor that the seller controls is the agent they select to represent them in the sale of the home. Selecting the "right" person to market your home is very important and worth careful consideration. Your agent will be the manager of the entire marketing process. They'll position your home to be competitive with the other homes in your price range and area while attracting the broadest range of buyers possible. Your agent will offer advice on what needs to be done before the property is offered for sale. Your agent can also offer recommendations for a variety of service providers if work needs to be done. There are a lot of professionals involved in the sale of a home like lenders, title officers, appraisers, inspectors, insurance agents, surveyors, and the buyer's agent, just to name a few. Your listing agent will coordinate the communications between the other professionals and negotiate directly with them. Your agent's role as third party negotiator is critical and you need to feel confident in their ability to serve your best interests.

A Seller's equity in their home is the difference between what the home is worth and what they owe. At any point in time, it is an estimation because value is a very subjective term. If the seller thinks the home is worth more than an actual buyer will pay for it, the estimated equity is too high. If a buyer is willing to pay more than the seller believes the home is worth, the estimated equity is too low.

A true determination of equity becomes more objective when the home is sold, and the value is solidified by the sales price. This value is determined by negotiations between a seller and buyer and eliminate speculation and conjecture because money and title are being exchanged. The equity being defined above is more accurately referred to as Gross Equity. After the ordinary and necessary expenses connected with the sale of a property are deducted from the sales price, along with any mortgage balance and/or liens, the proceeds are referred to as Net Equity. Like in business, the goal is to maximize revenue and minimize expenses, the same is true in selling a home. The goal is to achieve the highest possible sales price while keeping the expenses as low as possible. Setting the price of a home is ultimately, the seller's decision. It is critical because not only will it impact the amount of proceeds the seller realizes, but it can also affect the length of time it takes to sell, how much activity it will generate from buyers, and eventually, whether it sells at all. The cost of a home is what the seller paid for it and the improvements made. Cost has no relationship to value. Market value is the most probable price willing and informed buyers and sellers can agree upon in a competitive market in a reasonable period. Price the home too low and the seller has unrealized proceeds. Price it too high and it eliminates interested buyers. Preparing the home to go on the market has expenses involved. Things like painting the front door or adding landscaping to increase the initial appeal is an investment to attract the buyer's attention. While it may not add value to the home, it is an important element. Decluttering the home takes time and may even involve temporarily renting a storage facility for things that may make your home feel smaller or detract from making your home as visually appealing as possible. There are obviously selling expenses involved in the sale of a home which can vary based on the price of the home, what is customary in your area and negotiations in the sales contract. Your agent can advise you on these so that you don't pay anything out of the ordinary and can provide you an estimate of what is to be expected. Your real estate professional can provide you the information necessary to decide on price. However, do not confuse your decision on whom to market your home by the price indicated by the market and reported by the agent. The market determines the value, and the seller sets the price. Your decision in selecting an agent should be based on trust, reputation, integrity, and the ability to execute a successful marketing plan. In today's market, on average, homes, are selling in 17 days and sellers are seeing an average of five offers. It is not uncommon for homes to sell for more than the list price, assuming they are not priced dramatically over the market initially. Discuss with your real estate professional pricing your home slightly below market value and using a "coming soon" promotion to encourage increased buyer interest and possibly, encourage multiple offers. 8/23/2021 0 Comments Understand Mortgage ForbearanceSome homeowners who could not afford to make their mortgage payments this past year have been relieved to find out that their mortgage servicer or lender allowed them to pause or possibly, reduce their payments for a limited period. While it does relieve the financial pressure, it is a temporary remedy.

About 2/3 of the people who entered forbearance during the pandemic have exited the program. There are only a little over two million homeowners remaining in forbearance. It is important for owners who find that they cannot make the payments on their mortgage to contact their lender and request a forbearance. If you stop making mortgage payments without a forbearance agreement, the servicer will report this information to the credit reporting companies, and it can have a lasting negative impact on your credit history. Without going through that process, the lender assumes you are delinquent, and protections afforded under forbearance may not apply. Forbearance does not forgive the money that is owed. The borrower must repay any missed or reduced payments in the future. If forbearance was issued under the CARES Act, the lender cannot require payment in full at the end of the forbearance. Additionally, Fannie Mae has declared "following forbearance, you are not required to repay missed payments all at once, but you have that option." The forbearance agreement issued by the lender allows a borrower to avoid foreclosure for a period until, hopefully, the borrower's financial situation improves. If at the end of the stated period, the borrower's hardship still exists, the lender may be able to extend the time frame. The provisions of the forbearance vary based on the type of mortgage. The lender can tell you the specific provisions and options. Loans made by Fannie Mae and Freddie Mac require lenders to suspend reports to credit bureaus of past due payments for borrowers in a forbearance plan and no penalties or late fees will be assessed. Furthermore, the lender is mandated to "work with the borrower on a permanent plan to help maintain or reduce monthly payment amounts as necessary, including a loan modification." At the end of the forbearance, there can be several options available to repay the suspended or paused amounts. You can resume your normal payment and repayment plan can be established. If you can start making the payment but can't afford additional payments, the missed payments could be added to the end of the loan or possibly, a secondary lien that is due and payable when you refinance, sell or terminate your mortgage. In cases where the borrower can't afford to make the regular payments, a loan modification may be available with lower payments, but the term would be extended. While the CARES Act does not require borrowers at the end of the forbearance period to repay skipped payments in a lump sum, if a borrower is able, they may do so. The purpose of this is to re-establish a payment plan that the borrower can repay the money owed. To be eligible for a loan modification, borrowers must show they cannot make the current mortgage payments because of financial hardship while demonstrating they can meet their obligations with the proposed restructured terms. Under the CARES Act, borrowers with a GSE-backed mortgage are entitled to an additional 180-day extension which would be a total of 360 days. It is necessary to contact the servicer/lender for the extension. There can be both legal and tax issues concerning in forbearance and professional advice is recommended. A list of U.S. Department of Housing and Urban Development approved Counseling agencies are available. There is a story of a real estate agent's prayer: "Dear Lord, if I can't be someone's first love, or second wife, at least, please let me be their third REALTOR®."

|

|  |  |

11/2/2020 0 Comments

6/15/2020 0 Comments

9/16/2019 1 Comment

5/28/2019 0 Comments

Weichert, Realtors

9299 Old Keene Mill Rd Burke, VA 22015 (703) 569-7870 |

Michele Brantley

(703)943-7003 michelesellsva@gmail.com Copyright © 2022 |

RSS Feed

RSS Feed